Once the market swooned on April 2, the selling opportunity flipped to a buying opportunity. Those that did nothing came out OK. Image: janews/Shutterstock.com

By: Abraham Grungold

Once the market swooned on April 2, the selling opportunity flipped to a buying opportunity. Those that did nothing came out OK. Image: janews/Shutterstock.com

By: Abraham GrungoldThe Thrift Savings Plan (TSP) has a 38-year history of success. It has been compared to many private sector index funds. Like many investments there are ups and downs in the market. Investors need to recognize those fluctuations and weather the storm of those market changes. A successful investor knows that time is on their side.

I am following up on my last article in April 2025, called TSP Buying Opportunities. The Trump Administration had a Tariff deadline of April 2, 2025. This had been causing a lot of hysteria in financial markets, and of course among TSP Investors.

TSP investors had sufficient warning to make their interfund investment changes – but the breadth and size of the tariffs announced caught many off guard. Instead, TSP investors PANICKED on April 2 and began asking for financial advice from Facebook Forum strangers. This created the new term “Panicans.” Anyone who moved their money after April 2 into the G Fund, recognized a loss. Accounts dropping in value after April 2 was a dip in the market and it became a buying opportunity – not a selling opportunity after the fact. Markets began to acclimate to the White House’s trade approach and investors poured back in, sending indexes higher.

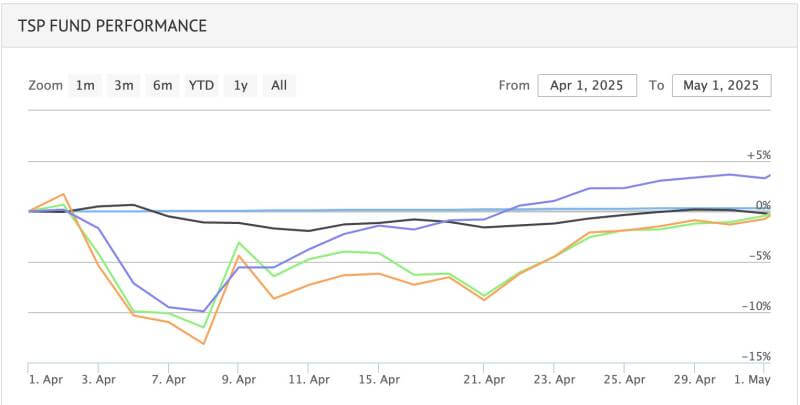

April 1 – May 1 2025

If these TSP investors did absolutely nothing, much of the depreciation had come back a few weeks later. So how has the TSP handled all the hysteria and what are the results.

- On April 2, the S&P 500 was 5633.

- On April 8, the S&P 500 was 5062, a decrease of 10%.

- On September 30, the S&P 500 was 6656, an increase of 18%.

- On January 1, 2025, the S&P 500 was 5868. The C Fund has grown 13% since September 30. Again, if TSP investors had done absolutely nothing during 2025 and not transferred their Fund shares into the G Fund, they would be having a great year.

During April and May 2025, I made purchases from my TSP G Fund into the C and S Funds. As a TSP investor you are allowed to make two interfund transfers each month. Watching the market and buying on the dip was my strategy during this Tariff Liberation Period.

During April 2 through September 30, my TSP balance increased by 22%. Presently, my wife has been encouraging me to perhaps take the profits and go back to the G Fund. Currently, I have decided to continue investing aggressively through 2026. But I will be watching the markets for any a usual activity or trends.

Now there is nothing wrong with being a 100 percent G Fund investor. You will simply not become a TSP millionaire if you are solely investing in the G Fund.

Investing methodically is a strategy that emotionally is not for every TSP investor, but certainly worth trying.

Using computer metrics, and taking advice from trolls in Facebook forums are not good strategies and usually it is a recipe for disaster.

Use the TSP website resources and look at what moments in history caused the TSP to drop in value. Learn from those historical moments and take advantage of those moments for buying opportunities.

As a TSP investor, during my 38 years, I have only made 2-3 major investment changes with my TSP. I carefully considered the positives and negatives of those changes and lived with my decisions without any regret.

As they say: No risk, no reward.

Abraham Grungold is a retired federal employee with 36 years of federal service – including with the USPS Inspector General, the VA Inspector General, the US Dept of Justice, and the US Dept of Labor. Through his company AG Financial Services he helps federal employees with their TSP and federal retirement planning and decisions. Mr. Grungold has written over 80 articles regarding the TSP and FERS retirement and been a guest on several podcasts with the Federal News Radio and Government Executive Magazine.

Conversions to Schedule P/C Pending; Acknowledgement Form Draws Attention

Federal Employee Survey Shows Plummeting Views on Engagement, Leadership, Performance

OPM Takeovers of RIF, Suitability Appeals Diminish Legal Rights, Unions Say

See also,

Calculating Service Credit for Sick Leave At Retirement

FERS Supplement vs The 10% Pension Bonus

How Your FERS, Social Security and TSP Payments Get Taxed