Medicare is a big program with lots of parts and this decision should not be treated lightly. Image: Asfia/Shutterstock.com

By: Dallen Haws

Medicare is a big program with lots of parts and this decision should not be treated lightly. Image: Asfia/Shutterstock.com

By: Dallen HawsIf you are nearing age 65 then you will be absolutely bombarded with phone calls and mailers trying to get you to buy all kinds of Medicare plans/supplements.

To add to the confusion, federal employees have FEHB (federal employee health insurance) which means that what most Americans do won’t apply to you.

With medical expenses being one of the most expensive parts of retirement, it is essential that federal employees get this one right.

I Have FEHB. Why Do I Need Medicare?

As a federal employee with FEHB you don’t need Medicare. You could stay on your FEHB plan for the rest of your life.

However, most federal employees get Medicare.

This is because having both Medicare and FEHB often creates great wrap-around benefits which means that you rarely have any out of pocket expenses in retirement.

However, the devil is in the details.

What is Medicare?

Medicare is a BIG program with lots of different parts and details.

However, 95% of federal employees should only worry about Medicare parts A and B.

Note: When federal retirees say they are “on Medicare”, they usually mean that they are on Medicare A and B.

Medicare A is free so that one is a no brainer at 65.

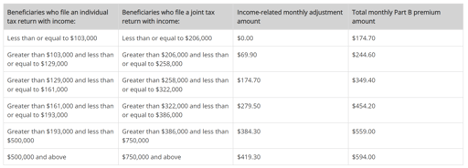

Medicare B is not free and the premium depends on your income per this chart below (2024 rates).

Most people will pay the base rate of $174.70 but your price will go up as your income does.

Note: The most common situation that I’ve seen where it not make sense to be on Medicare part B is when the person had very high income which would make the premiums not worth it.

The Most Common Strategy

The most common strategy that I’ve seen is when federal employees keep their FEHB and enroll in Medicare A and B.

This combination can offer very comprehensive coverage.

However, not all FEHB plans play well with Medicare.

Some FEHB plans will pay you hundreds of dollars a year to help reimburse part of the cost of Medicare part B while others don’t give you any benefit for being on Medicare.

The most successful retirees that I’ve seen enroll in Medicare A and B while finding a FEHB that works well with Medicare.

FEHB is your Supplement

Non-federal employee Americans often get some sort of Medicare supplement or Medigap plan to supplement Medicare A and B.

However, for most federal employees their FEHB plan serves this same role and they don’t need another Medicare supplement.

Part B Penalty

If you choose to not enroll in Part B when you turn 65 but enroll later then you will be subject to a 10%/year penalty.

Basically, for every year that you waited to enroll, your premiums will be 10% higher if you ever wanted to enroll later.

But of course if you never enroll in Part B then this penalty will never affect you.

Note: The clock for this penalty doesn’t start until you retire if you work beyond age 65.

When to Enroll in Medicare?

If you are already retired at age 65 then most enroll in A and B at 65.

However, for those that work beyond 65, most enroll in Medicare A at 65 and wait to enroll in Part B until retirement.

Note: One reason to not enroll in Medicare A at 65 if you are still working is if you are in a HDHP (high deductible plan) and using an HSA. You can not contribute into an HSA and be on Medicare so delaying Medicare A enrollment enrollment until retirement would give you more time to contribute to an HSA.

Don’t Forget Part D!

Medicare part D covers prescription drugs. However, up to this point (pre-2024) there has been no point for federal employees to enroll in part D as all FEHB plans already had the same or better drug coverage and part D would cost extra.

However, this has changed recently with some recent legislation that has made part D more attractive for those with high out of pocket drug costs.

Summary: Most federal employees still don’t need Medicare part D but you’ll want to give it a thorough look if you have regular high out of pocket expenses for your prescription drugs.

Final Thoughts

Medicare is a big program with lots of parts and this decision should not be treated lightly.

If you are approaching age 65 then I recommend educating yourself thoroughly and what is out there so you can go into retirement with confidence.

Afterall, having great health coverage at a reasonable cost is key to a great retirement.

Dallen Haws is a Financial Advisor who is dedicated to helping federal employees live their best life and plan an incredible retirement. He hosts a podcast and YouTube channel all about federal benefits and retirement. You can learn more about him at Haws Federal Advisors.

Nearly 10,000 Federal Offices Don’t Meet Usage Standards

Conversions to Schedule P/C Pending; Acknowledgement Form Draws Attention

OPM Plan on Employee Ratings Asking for Abuse, Says Senior House Democrat

OK, FERS and TSP, but What About Social Security Retirement Income?

See also,

Calculating Service Credit for Sick Leave At Retirement

FERS Supplement vs The 10% Pension Bonus

How Your FERS, Social Security and TSP Payments Get Taxed